How to Manage Finances in 2026: The Ultimate Guide to U.S. Wealth in the AI Era

In 2026, the American financial landscape is undergoing a radical shift. We have moved past the era of manual spreadsheets into the age of AI-driven wealth orchestration. With the Federal Reserve expected to stabilize interest rates between 3.0% and 3.25% and inflation cooling to roughly 2.7%, managing your money in the United States now requires a blend of high-tech tools and timeless strategic discipline.

This guide provides a comprehensive roadmap for navigating personal finance in 2026, specifically tailored for the U.S. economy.

1. The 2026 Economic Context: Stability with a “No-Hire” Twist

To manage your money well, you must understand the current climate. The U.S. economy is in a “soft landing” phase. While inflation is no longer the monster it was in 2023, the labor market has shifted to a “low-hire, low-fire” dynamic.

This means while your job is likely safe, finding a new one may take longer. Consequently, your emergency fund strategy must evolve. In 2026, the standard three-month buffer is being replaced by a six-to-nine-month liquidity ladder to account for a slower hiring cycle.

When looking for the best savings accounts 2026, prioritize those offering high-yield cash management features that integrate with your primary checking.

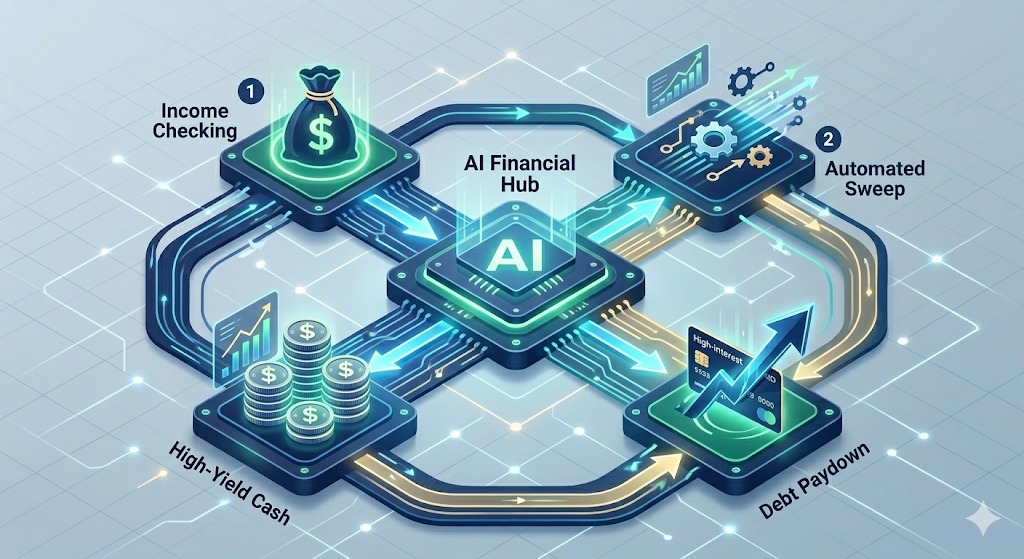

2. Leveraging AI for Automated Wealth Management

The biggest change in 2026 is the mainstream adoption of AI Financial Agents. These aren’t just chatbots; they are autonomous tools that monitor your accounts in real-time.

How to use AI for Budgeting:

- Hyper-Personalized Nudges: Modern apps now use “predictive spending” to alert you before you overspend, based on your historical Tuesday afternoon coffee runs or weekend trips.

- Subscription Pruning: AI agents now automatically identify and cancel “zombie subscriptions” that have gone unused for 60 days.

- Automated Sweep Accounts: Use tools that automatically “sweep” any balance over your designated “operating cash” into a money market fund or a CD ladder to capture every cent of interest.

3. The 2026 Investment Strategy: Resilience and Real Assets

With the S&P 500 continuing to show strength but valuations remaining high, U.S. investors are pivoting toward portfolio resilience.

The “Belly of the Curve” Strategy

Financial advisors in 2026 are focusing on the “belly of the yield curve”—specifically 3-to-7-year Treasury bonds. As the Fed pauses its rate-cutting cycle, locking in these mid-term yields provides a stable income stream while protecting against potential market volatility later in the decade.

Diversification Beyond “The Magnificent Seven”

While tech remains dominant, 2026 is the year of active management. Look toward:

- Infrastructure & Energy: Specifically U.S.-based renewable and grid-modernization firms.

- Real Assets: Using fractional real estate platforms to hedge against any residual inflation.

- Tax-Equivalent Yields: For high-income earners, municipal bonds remain a cornerstone of U.S. tax-efficient investing.

4. Tax Planning and the 2026 Midterm Shift

In the U.S., 2026 is a midterm election year, which often brings “policy noise.” Strategically, you should focus on what you can control: Tax-Advantaged Accounts.

- Roth Conversions: If you expect higher tax rates in the future, 2026 is a prime year to consider a partial Roth IRA conversion while rates are relatively predictable.

- HSAs as Retirement Vehicles: The Health Savings Account (HSA) remains the most powerful tax tool in the U.S. code. Maximize this first to get the “triple tax advantage” (tax-free contributions, growth, and withdrawals).

5. Debt Management: Consolidation is Key

High interest rates on credit cards remain a significant drag on American households. The 2026 strategy is aggressive consolidation.

If you are carrying high-interest debt, explore Personal Loans or HELOCs (Home Equity Lines of Credit), which currently offer significantly lower rates than the average 20%+ credit card APR. Use an AI-driven debt payoff calculator to determine if the “Snowball” or “Avalanche” method is more efficient for your specific interest rate spread.

Frequently Asked Questions (FAQ)

1. What are the best budgeting apps for 2026?

The top-rated apps in 2026 are those that offer embedded finance—meaning they don’t just track your money, but actually move it for you. Look for platforms like Copilot, Origin, or Fidelity’s Digital Tools, which offer AI-driven variance analysis.

2. Should I still invest in the stock market if a recession is possible?

Yes. Historically, trying to “time the market” results in lower returns than “time in the market.” In 2026, focus on Dollar-Cost Averaging (DCA) into low-cost index funds to smooth out volatility.

3. How much should I save for taxes if I am a freelancer in 2026?

The general rule of thumb for U.S. freelancers is to set aside 30% of your gross income. With the potential for changing tax brackets, it is safer to over-save and receive a refund than to be caught short during quarterly estimated payments.

4. Is it better to pay off my mortgage or invest extra cash in 2026?

This depends on your mortgage rate. If you locked in a rate below 4% during the pandemic, you are likely better off investing extra cash in a High-Yield Savings Account (HYSA) or the stock market. If your rate is above 6%, a guaranteed return by paying down principal may be more attractive.